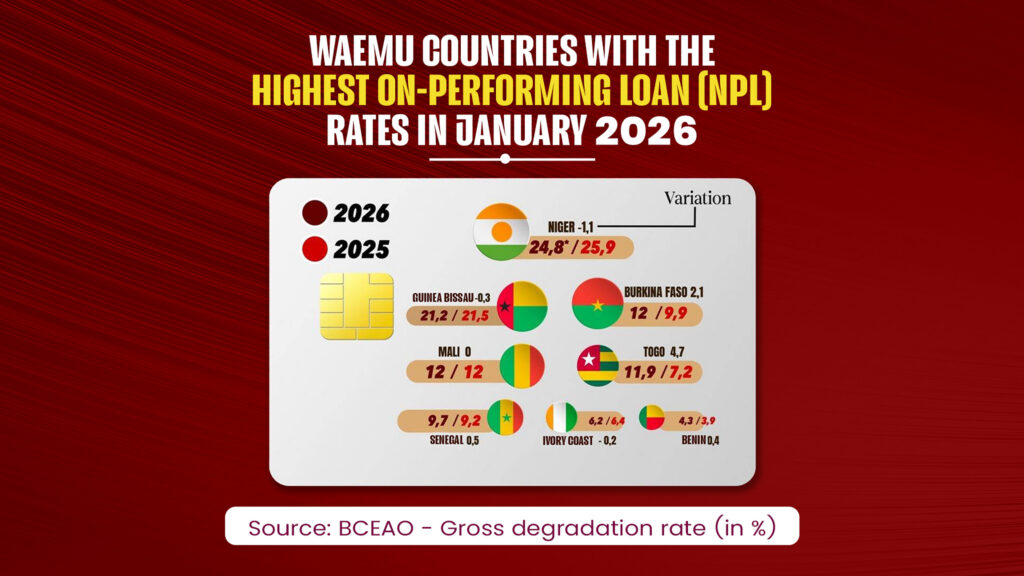

The UEMOA’s latest January 2026 economic outlook paints a stark picture: while the region’s banking sector achieves symbolic milestones, it is increasingly undermined by a surge in financial risks. At the epicenter of this turmoil, Niger stands out with a record non-performing loan (NPL) rate, symbolizing a widening regional divide.

The Niger Factor: A Distress Signal in Regional Banking

Despite efforts to stabilize the West African economic bloc’s financial system, Niger remains the most vulnerable link. Its banking sector’s performance continues to lag far behind regional peers, even as other indicators show marginal improvement.

Record-High NPLs: A Disturbing Trend

Niger’s NPL rate has surged to 24.8% as of January 2026, cementing its position as the worst-performing economy in the union. This means nearly one in four loans issued in Niger is now in default—far exceeding acceptable thresholds.

Structural Flaws Expose the Economy

While the rate has dipped slightly from 25.9% in 2025, the gap between Niger’s figures and the regional average highlights an acute vulnerability. Persistent security threats and political instability have exacerbated financial fragility, leaving the country exposed to systemic shocks.

A Tale of Two Blocs: Coastal Stability vs. Sahelian Struggles

January 2026 data underscores a clear divide within UEMOA: coastal economies demonstrate resilience, while Sahelian nations face escalating financial distress.

Sahelian Economies Under Pressure

- Mali and Burkina Faso: Both nations report NPL rates of 12%, with Burkina Faso experiencing a sharp year-on-year increase of 2.1 percentage points.

- Guinea-Bissau: Remains in critical territory with an 21.2% NPL rate, signaling severe financial strain.

Coastal Economies: Relative Stability, Select Weaknesses

The bloc’s coastal states maintain stronger loan portfolios, though exceptions persist:

- Benin: Leads the union with the lowest NPL rate at 4.3%, setting a benchmark for financial prudence.

- Côte d’Ivoire & Senegal: Show moderate stability with rates of 6.2% and 9.7%, respectively.

- Togo’s Outlier Status: Defies regional trends with a dramatic spike in NPLs, jumping from 7.2% to 11.9% (+4.7 points).

Credit Growth Stalls Amid Rising Concerns

The UEMOA’s total loan portfolio has surpassed 40.03 trillion FCFA—a historic high (+4.7% year-on-year)—but momentum appears to be waning. The surge in bad loans has cast a long shadow over this achievement.

Bad Loans Skyrocket to Alarming Levels

Non-performing loans have ballooned to 3.63 trillion FCFA, while the coverage ratio has plummeted to 59%. Banks are struggling to keep pace with provisioning demands, raising alarms over liquidity risks.

Banks Retreat: Tighter Lending and Risk Aversion

In response to Niger’s escalating defaults and broader regional instability, financial institutions are adopting defensive strategies:

- Stricter Loan Criteria: Higher personal contributions and collateral requirements are now standard.

- Selective Credit Expansion: Banks prioritize balance sheet safety over lending growth, risking reduced funding for local SMEs and SMBs.

As of early 2026, the UEMOA banking system stands at a crossroads. While the bloc’s overall stability remains intact, Niger’s crisis and the spread of financial risks across the Sahel demand urgent attention to avert a potential liquidity crunch.